The 30-second pitch

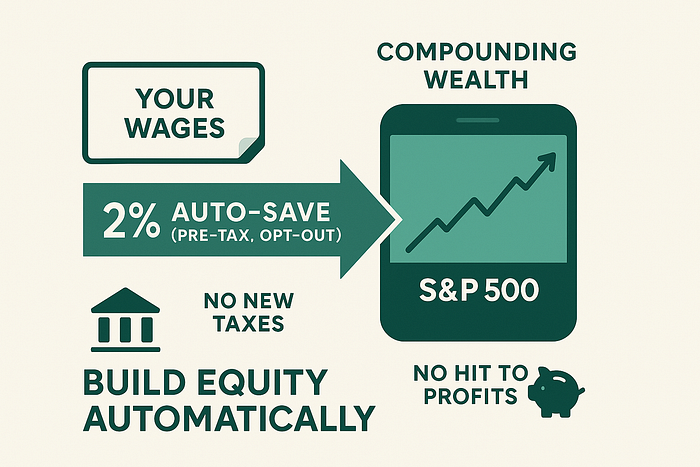

- Default ownership. Two percent of every paycheck is automatically diverted — pre-tax, opt-out — into the worker’s personal, low-fee S&P 500 index fund.

- No new taxes. Neither corporate profits nor government budgets are touched; wealth grows through compounding, not redistribution.

- Everyone wins. Households build equity, companies keep capital, and the public sector still collects ordinary sales-tax revenue when rising balances eventually get spent.

In one line: Let paychecks buy stock by default, so every worker builds equity while they build the economy.

Why we need something simpler than UBI

Universal Basic Income is elegant on paper but politically heavy: it demands new taxes, rewrites the safety-net, and risks dulling the incentive to work. CED flips the script:

UBI CED Up-front transfers, funded by higher taxes or deficits Self-funded ownership, no new public spending Possible work-disincentive Keeps the “skin-in-the-game” link between labor and reward Government decides the benefit size Households capture open-ended market upside

CED isn’t welfare; it’s forced-savings with a “default yes” switch.

How the mechanics work

- Payroll rails — Employers (or gig platforms) route 2 % of gross wages into the worker’s brokerage account.

- Opt-out, not opt-in — Behavioral-finance research shows default enrollment boosts participation from ~30 % to 90 % in 401(k)s. The same psychology powers CED.

- Ultra-low fees — Vanguard-style index funds (< 0.05 % expense ratios) preserve compounding.

- Portability — Change jobs, keep the account; the contribution switch rides along with your SSN.

- Withdrawal rules — Treat the balance like a Roth IRA after a five-year holding period: free to tap for retirement — or sooner for first-home, medical, or education costs.

A quick numeric gut-check

If someone earned $50,000 every year from 2000–2025 and CED skimmed $1,000 into an S&P 500 fund annually, what would that be worth?

Using the index’s total-return CAGR (~8 % over that span), 25 equal $1 k deposits compound to ≈ $73 k — about 1.5× a single year’s salary, produced with zero lifestyle change.

Scale that across 150 million workers and you build $11 trillion in broad-based household equity within one generation.

But what about people living paycheck-to-paycheck?

- Default, not mandate. Anyone can opt out with a single checkbox if the 2 % truly breaks the budget.

- Earned-income match. States could sweeten the pot for the lowest quintile (e.g., dollar-for-dollar match on the first $200/year) without opening a federal spigot.

- Financial-literacy nudge. A balance that updates every payday is the best personal-finance teacher on Earth.

Corporate impact: essentially neutral

CED doesn’t skim profits; it skims wages before they’re taxed or spent. Employers see no new cash expense, only a minor payroll-software tweak — much easier to pass politically than a 2 % corporate-tax hike.

Precedents that prove it’s doable

- Australia’s Superannuation (10.5 % mandatory)

- U.S. 401(k)/403(b) auto-enrollment (3–6 %)

- UK NEST pension (8 % default)

CED is simpler — just one flat, low percentage and one broad index fund.

Implementation roadmap

- Amend the Tax Code: classify CED deposits as “CED-401h” contributions — pre-tax in, tax-free growth, Roth-style qualified withdrawals.

- One national clearinghouse: think “FedNow for equities,” minimizing administrative overhead.

- Default starts at 2 %: raise only if wages stagnate relative to market returns.

- Quarterly public dashboard: transparency keeps trust high; everyone sees aggregate balances grow.

The big picture

- Post-scarcity alignment. As AI and automation drive marginal production costs toward zero, capital ownership — not labor income — captures most gains. CED puts that capital in everyone’s pocket.

- Political palatability. Left applauds wealth-building for all; right appreciates zero new taxes and personal responsibility.

- Resilient middle class. By 2050 a typical 25-year-old could retire with a seven-figure nest egg — even if real wages plateau.

What’s next?

- Run pilot programs with federal employees or large gig-platforms.

- Pair CED with a “rainy-day loan” feature so low-income workers can temporarily tap contributions instead of opting out.

- Offer micro-match vouchers funded by corporate philanthropy — turn ESG talk into tangible stakes for workers.

TL;DR

Citizen Equity Dividend is the simplest wealth engine nobody’s using. Two percent of each paycheck buys broad-market equity by default, letting compounding do the heavy lifting. No new taxes, no corporate haircut — just ownership at scale. In a future where productivity soars but wage growth may not, CED ensures every worker still shares the upside.

So — what do you think?

Is a tiny, opt-out stock purchase the missing gear in America’s wealth machine, or does it leave too much to individual fortune? Let’s debate in the comments.